Part 1: Identification of Business Functions

Part 1: Identification of Business Functions

CBF 1: Risk Assessment and Guarantee Issuance

Part 1: Identification of Business Functions

In any organisation that engages in financial guarantees or credit risk mitigation, the function of Risk Assessment and Guarantee Issuance plays a pivotal role in safeguarding institutional integrity and ensuring sustainable operations.

This critical business function encompasses a series of interconnected processes—from initial application intake to post-issuance monitoring—each vital to the timely and secure issuance of guarantees.

Understanding and defining the Minimum Business Continuity Objective (MBCO) for each sub-function within this process is essential to maintaining service delivery during disruptions.

This chapter breaks down the sub-critical business functions (CBFs) involved in Risk Assessment and Guarantee Issuance and presents them in a structured format, aligning each with its corresponding MBCO.

The MBCO serves as a benchmark for the maximum allowable downtime that a business unit can tolerate before significant operational, financial, or reputational damage occurs.

The content is grounded in principles outlined by BCM Institute and aligns with industry best practices in business continuity planning.

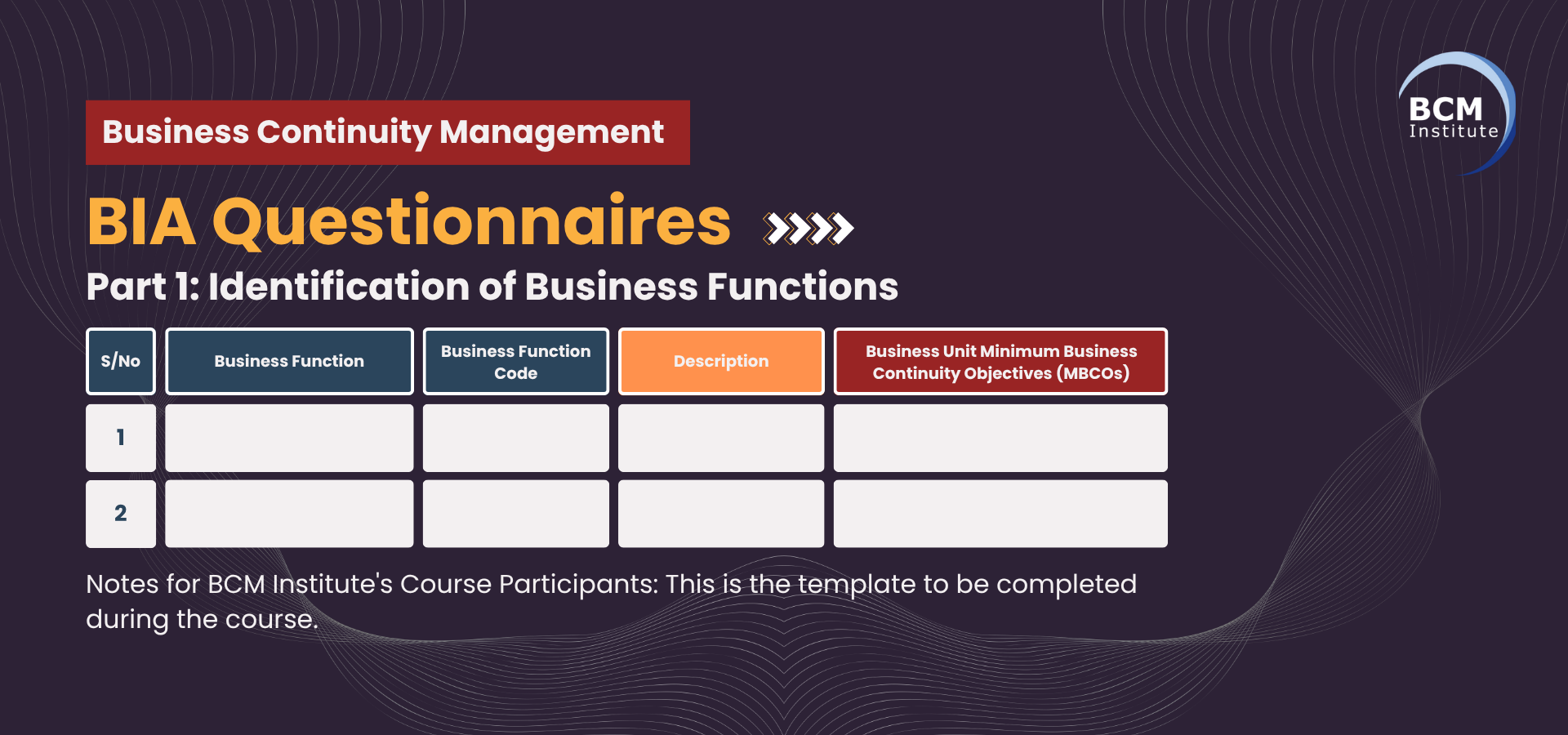

Table 1-1: [BIA] [P1] Identification of Business Functions for CBF 1: Risk Assessment and Guarantee Issuance (Sub-CBF)

Business Unit MBCO

|

Critical Business Functions (CBF) |

CBF Code |

Description of CBF |

Business Unit Minimum Business Continuity Objective (MBCO) |

|

Application Intake |

CBF-RA-01 |

Receiving and logging applications for guarantees, ensuring all necessary documentation is collected for processing. |

Resume within 4 hours to prevent a backlog and maintain service levels. |

|

Preliminary Eligibility Check |

CBF-RA-02 |

Assessing applications against predefined criteria to determine initial eligibility for guarantee issuance. |

Resume within 8 hours to ensure timely processing of applications. |

|

Credit Risk Assessment |

CBF-RA-03 |

Evaluating the creditworthiness of applicants to assess potential risks associated with guarantee issuance. |

Resume within 12 hours to maintain risk assessment timelines. |

|

Site Visits / Due Diligence (if required) |

CBF-RA-04 |

Conducting on-site evaluations or additional due diligence for high-risk or significant guarantee applications. |

Resume within 24 hours to avoid delays in critical assessments. |

|

Guarantee Structuring |

CBF-RA-05 |

Designing the terms and conditions of the guarantee, including amount, duration, and obligations. |

Resume within 12 hours to proceed with timely approvals. |

|

Approval Process |

CBF-RA-06 |

Reviewing and approving the structured guarantee through appropriate authority levels. |

Resume within 8 hours to prevent bottlenecks in issuance. |

|

Issuance of Guarantee |

CBF-RA-07 |

Formalising and issuing the guarantee document to the applicant, ensuring legal and procedural compliance. |

Resume within 4 hours to meet contractual obligations. |

|

Post-Issuance Monitoring Setup |

CBF-RA-08 |

Establishing monitoring mechanisms to track compliance and performance related to the issued guarantee. |

Resume within 24 hours to ensure ongoing oversight and risk management. |

These MBCOs are indicative and should be validated through a comprehensive Business Impact Analysis (BIA) to align with your organisation's specific operational priorities and risk thresholds.

Summing Up ... for Part 1

A robust continuity strategy hinges on the identification of critical functions and the precise articulation of their Minimum Business Continuity Objectives.

The detailed breakdown of sub-CBFs under Risk Assessment and Guarantee Issuance provides organisations with a practical framework to prioritise response and recovery efforts during disruptive incidents.

By assigning specific MBCO thresholds to each step in the process, business units can ensure continuity in delivering essential financial services, uphold trust with clients and stakeholders, and mitigate regulatory and operational risks.

Ultimately, integrating these MBCO-aligned CBFs into the broader business continuity management (BCM) framework strengthens organisational resilience and enhances the ability to adapt in a rapidly evolving risk landscape.

CBF 1: Risk Assessment and Guarantee Issuance

Part 2: Impact Area Of Business Functions

The Risk Assessment and Guarantee Issuance process is one of the most critical operational pillars of Credit Guarantee Corporation Malaysia (CGC).

As a financial institution entrusted with facilitating credit access for micro, small, and medium enterprises (MSMEs), CGC’s ability to assess, structure, and issue credit guarantees efficiently and reliably directly influences its financial viability and reputation.

This chapter provides a comprehensive impact assessment of each sub-function within the Risk Assessment and Guarantee Issuance process. It outlines the potential financial losses, operational disruptions, and strategic risks that could arise from failures or delays in these activities.

The objective is to inform business continuity planning and ensure that necessary safeguards and response strategies are in place to maintain CGC’s service levels, compliance posture, and stakeholder trust during any adverse event.

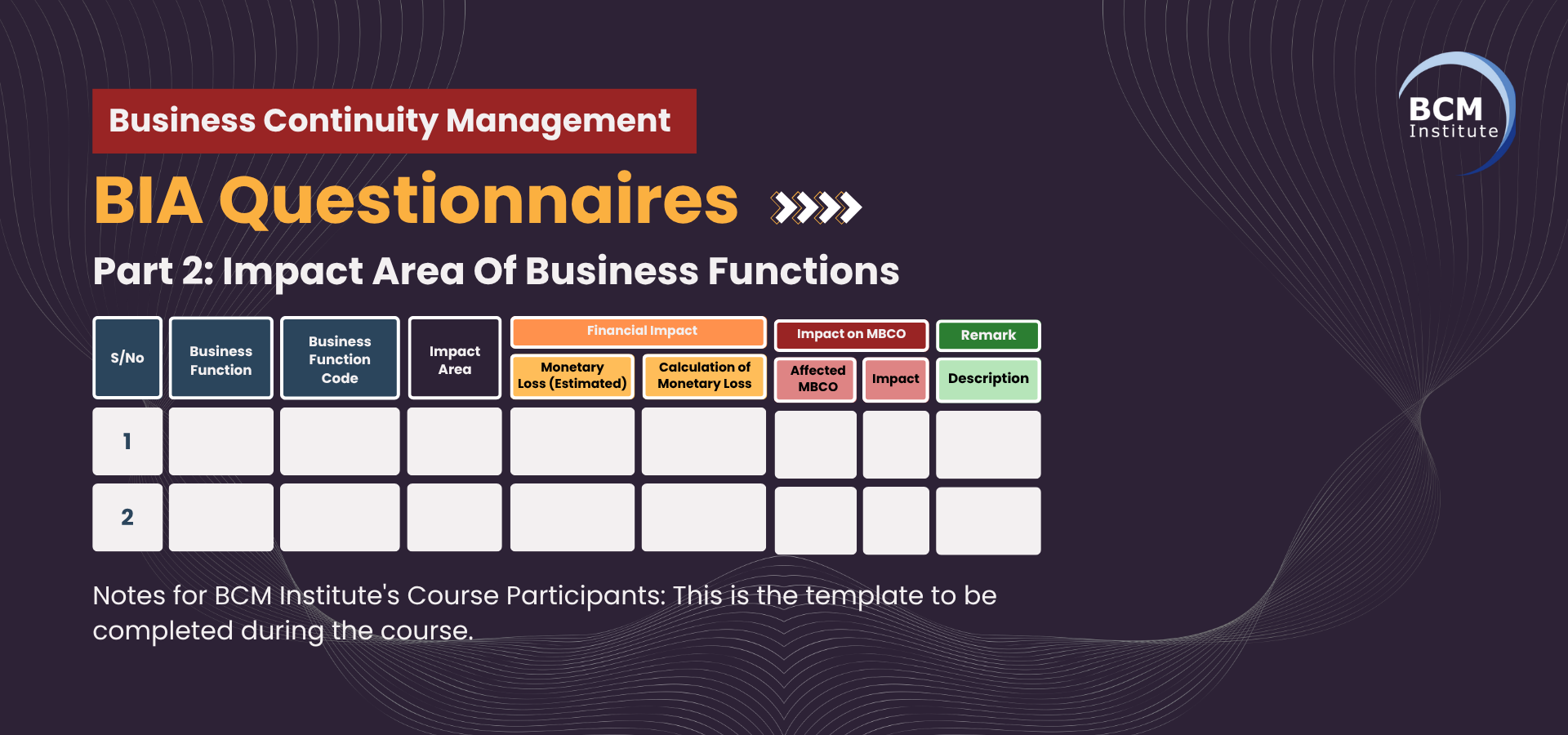

Table 2-1: [BIA] [P2] Impact Area Of Business Functions for CBF 1: Risk Assessment and Guarantee Issuance

|

Critical Business Function |

Critical Business Function Code |

Impact Area |

Financial Impact - Monetary Loss (Estimated) |

Financial Impact - Calculation of Monetary Loss (State Formula for Calculations) |

Impact on MBCO - Affect MBCO |

Impact on MBCO - Impact |

Remarks - Description |

|

Application Intake |

RAGI-01 |

Financial, Processes, Reputation |

RM 500,000 |

(Average daily applications × Potential guarantee value per application) × % of missed opportunities × 7 days |

Guarantee Processing |

Delays in application intake can lead to missed opportunities, affecting CGC's ability to support MSMEs timely. |

Prolonged unavailability may damage CGC's reputation as a reliable guarantor, leading to loss of trust among financial institutions and MSMEs. |

|

Preliminary Eligibility Check |

RAGI-02 |

Financial, Legal and Regulatory |

RM 300,000 |

(Number of applications × % ineligible × Potential default cost) × 7 days |

Risk Assessment |

Failure in eligibility checks can result in high-risk guarantees being approved, increasing potential defaults. |

Inadequate checks may lead to non-compliance with regulatory standards, risking legal penalties and operational sanctions. |

|

Credit Risk Assessment |

RAGI-03 |

Financial, Legal and Regulatory, Reputation |

RM 1,000,000 |

(Number of assessments × Average guarantee amount × Default probability) × 7 days |

Risk Management |

Inaccurate risk assessments can lead to high default rates, impacting CGC's financial stability. |

Poor risk assessment processes can erode stakeholder confidence and may attract regulatory scrutiny. |

|

Site Visits / Due Diligence |

RAGI-04 |

Financial, Processes, Reputation |

RM 200,000 |

(Number of site visits × Cost per visit) + (Potential losses from undetected risks) × 7 days |

Due Diligence |

Skipping due diligence can result in undetected risks, leading to financial losses. |

Neglecting site visits may compromise the integrity of the guarantee process, affecting CGC's credibility. |

|

Guarantee Structuring |

RAGI-05 |

Financial, Legal and Regulatory |

RM 400,000 |

(Number of guarantees × Potential structuring errors × Average loss per error) × 7 days |

Product Development |

Improper structuring can lead to unenforceable guarantees, resulting in financial losses. |

Errors in guarantee structuring may lead to legal disputes and regulatory non-compliance. |

|

Approval Process |

RAGI-06 |

Financial, Processes |

RM 600,000 |

(Number of pending approvals × Average guarantee amount × Opportunity loss rate) × 7 days |

Decision Making |

Delays in approvals can hinder MSME financing, affecting CGC's operational efficiency. |

Inefficient approval processes may lead to bottlenecks, reducing CGC's responsiveness to market needs. |

|

Issuance of Guarantee |

RAGI-07 |

Financial, Legal and Regulatory, Reputation |

RM 800,000 |

(Number of guarantees × Average guarantee amount × Delay penalty rate) × 7 days |

Service Delivery |

Delays in guarantee issuance can breach service level agreements, leading to penalties. |

Timely issuance is critical to maintain trust with financial institutions and MSMEs. |

|

Post-Issuance Monitoring Setup |

RAGI-08 |

Financial, Processes, Legal and Regulatory |

RM 350,000 |

(Number of active guarantees × Monitoring failure rate × Average loss per failure) × 7 days |

Compliance Monitoring |

Inadequate monitoring can result in undetected defaults, increasing financial risks. |

Effective monitoring ensures compliance and early detection of potential defaults, safeguarding CGC's interests. |

Note: The financial impact estimates are illustrative and should be validated with actual operational data. The formulas are based on BCMpedia's guidelines for calculating financial impacts in business continuity planning.

Summing Up ... for Part 2

In summary, the Risk Assessment and Guarantee Issuance function encompasses several interdependent sub-processes that collectively shape CGC’s capacity to deliver on its mandate.

Disruptions in any of these areas—ranging from application intake to post-issuance monitoring—can have cascading effects on financial performance, regulatory compliance, and organisational credibility.

By quantifying the monetary loss estimates and understanding the broader impact on mission-critical business operations (MBCO), CGC can prioritise resilience-building initiatives, allocate resources efficiently, and embed proactive risk management into its operational framework.

This analysis serves as a foundational element in fortifying CGC’s business continuity strategy and sustaining confidence among its partners and beneficiaries.

More Information About Business Continuity Management Courses

To learn more about the course and schedule, click the buttons below for the BCM-300 Business Continuity Management Implementer [BCM-3] and the BCM-5000 Business Continuity Management Expert Implementer [BCM-5].

![Register [BL-B-3]*](https://no-cache.hubspot.com/cta/default/3893111/ac6cf073-4cdd-4541-91ed-889f731d5076.png)

![FAQ [BL-B-3]](https://no-cache.hubspot.com/cta/default/3893111/b3824ba1-7aa1-4eb6-bef8-94f57121c5ae.png)

![Email to Sales Team [BCM Institute]](https://no-cache.hubspot.com/cta/default/3893111/3c53daeb-2836-4843-b0e0-645baee2ab9e.png)